The $30 Trillion End Game: Inside the Proposed Fiscal-Monetary Accord

The era of the "Volcker Fed" is effectively over. We are witnessing the dismantling of the firewall between the US Treasury and the Federal Reserve, not by law, but by the sheer gravitational force of a $38 trillion debt load.

For fifteen years, we operated under the assumption that central bank independence was sacrosanct. That assumption is now a liability. Kevin Warsh’s nomination and his subsequent advocacy for a "new Accord" is not merely a policy tweak; it is a fundamental restructuring of the US sovereign balance sheet.

We are moving from a regime of inflation targeting to a regime of debt service targeting. For investors, this changes the physics of capital allocation. If you are still modeling risk based on the Taylor Rule, you are solving for a variable that no longer matters.

Here is the analysis of the proposed Fiscal-Monetary Accord and why it signals the end game for the free market in government bonds.

Kevin Warsh and the Blueprint for Unified Liability Management

The media frames the tension between the White House and the Federal Reserve as a political soap opera. They miss the structural reality: The Fed can no longer conduct monetary policy in a vacuum when the Treasury must roll over $10 trillion in debt annually.

Deconstructing the "Warsh Doctrine"

Kevin Warsh has long criticized the Fed’s "bloated" balance sheet. His solution, however, is not a return to 1990s orthodoxy, but a shift toward Unified Liability Management (ULM). Under this framework, the Treasury’s issuance strategy (what bonds it sells) and the Fed’s balance sheet strategy (what bonds it buys or holds) are treated as a single sovereign liability.

Currently, the Treasury often issues long-dated bonds (locking in high rates) while the Fed fights inflation by raising short-term rates. They are working at cross-purposes, costing the taxpayer billions. The Warsh Doctrine proposes ending this schizophrenia. It implies that the Fed’s balance sheet will no longer be used solely for economic stimulus (QE), but as a tool to actively manage the duration risk of the Treasury.

Moving beyond Quantitative Easing

This is not QE. Quantitative Easing was an "emergency" measure to inject liquidity. The new Accord represents a permanent structural shift where the central bank explicitly manages the yield curve to ensure debt sustainability.

The difference is intent:

- QE: "We are buying bonds to lower unemployment."

- The Accord: "We are capping yields because the Treasury cannot afford market rates."

Echoes of 1951: Revisiting the Treasury-Fed Accord

To understand where we are going, we must look at the last time the US debt-to-GDP ratio exceeded 100%.

Lessons from the WWII peg

During World War II, the Fed capped long-term Treasury yields at 2.5% to finance the war effort. The 1951 Treasury-Fed Accord was signed to break this peg, granting the Fed independence to fight the post-war inflation. It was the birth of the modern, independent central bank.

Why the 1940s playbook is back

Today, we are reversing the 1951 logic. In 1951, the austerity solution was politically viable because the debt was war-related—temporary and self-liquidating. Today’s debt is structural, driven by entitlements and compounding interest.

We are facing a math problem that politics cannot solve. With interest expenses now rivaling the defense budget, the "independence" of the Fed is a luxury the Treasury can no longer afford. The table below outlines the stark differences between the two eras.

Mechanics of Yield Suppression in a $38 Trillion Market

How do you cap yields without triggering hyperinflation? This is the technical heart of the proposal.

Targeting the long end of the curve

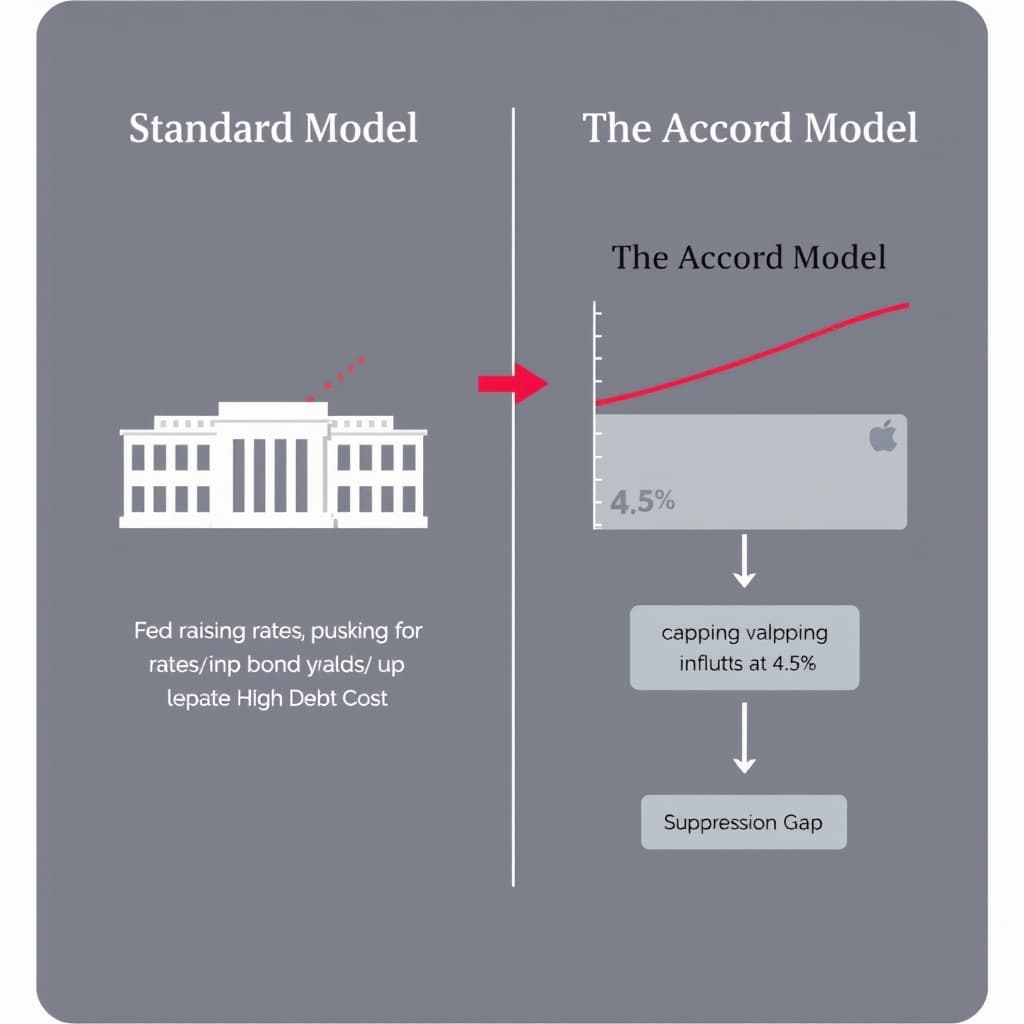

The Fed doesn't need to buy everything. It only needs to signal a "credible threat" to buy unlimited bonds at a specific yield (e.g., 4.5% on the 10-year). This is Yield Curve Control (YCC). By pinning the long end, the Fed allows the Treasury to issue long-duration debt at negative real rates, effectively inflating away the debt burden over a decade.

The mathematical necessity of capping real rates

The equation is simple: $r < g$.

- $r$ = Interest rate on debt.

- $g$ = Nominal GDP growth.

If $r$ stays higher than $g$, the debt spirals exponentially until default. The only way to stabilize the system without default is to force $r$ below $g$. Since the Fed cannot easily conjure GDP growth ($g$), it must forcibly suppress interest rates ($r$).

The Death of Autonomy: When Fiscal Dominance Takes Over

This is the end of the "risk-free" rate. When the price of money is fixed by a committee to aid the Treasury, the bond market ceases to be a price discovery mechanism and becomes a policy instrument.

Eroding the firewall

The risk is not just economic; it is institutional. If the Treasury Secretary can effectively dictate the Fed's balance sheet policy, the dollar loses its status as a politically neutral store of value. We are seeing the "emerging market-ification" of US institutional norms.

Long-term risks to the dollar

If the Fed becomes the permanent buyer of last resort, the volatility that is suppressed in the bond market will inevitably leak out into the currency market. You cannot suppress volatility; you can only transfer it. By fixing the price of bonds, the Accord transfers the volatility to the US Dollar.

Map of Incentives: Who Wins, Who Bleeds?

Understanding the Accord requires following the money.

- The Treasury (Winner): Gets to fund massive deficits at below-market rates. The "Suppression Gap" is a direct transfer of wealth from savers to the government.

- Equity Holders (Winner): "Financial Repression" forces capital out of bonds (which yield nothing in real terms) and into scarce assets like stocks, real estate, and crypto.

- Pension Funds & Savers (Loser): They hold the bag. They are paid 4% while inflation runs at 5-6%. They are the source of the subsidy.

- The Dollar (Loser): Becomes the release valve for global capital that demands a real return.

What Would Change My Mind?

I am betting on the Accord because the math leaves no other option. However, two scenarios could invalidate this thesis:

- A Productivity Miracle: If AI drives US GDP growth to 5-6% real, the denominator grows fast enough to stabilize the debt without repressing rates.

- Volcker 2.0: Kevin Warsh (or his successor) chooses to crash the economy and force a sovereign default rather than monetize the debt. Given the political suicide this entails, I view this as a near-zero probability.

Formal coordination is inevitable

The "Warsh Accord" is not a conspiracy; it is a balance sheet necessity. The US government cannot service $38 trillion in debt at true market rates.

Investors must stop waiting for the Fed to "pivot" back to normal. There is no normal. We are entering a period of state-managed bond prices. The play is not to fight the Fed, but to own the assets that the Fed cannot print.

Sources

- Federal Reserve History: The 1951 Treasury-Fed Accord

- US Congressional Budget Office: Long-Term Budget Outlook

- Hoover Institution: Kevin Warsh on Fiscal-Monetary Coordination

- US Department of the Treasury: Debt to the Penny

FAQ

What is the primary goal of a Fiscal-Monetary Accord?

The primary objective is to artificially suppress government borrowing costs (bond yields) to ensure the national debt remains serviceable, effectively subordinating monetary policy to fiscal needs.

How does this differ from standard Quantitative Easing (QE)?

While QE involves purchasing bonds to stimulate the economy or provide liquidity, a Fiscal-Monetary Accord explicitly targets specific yield caps to facilitate Treasury funding, regardless of inflation conditions. QE is often temporary; the Accord is structural.

Related

View all →