The $30 Trillion Pivot: Why Banks Are Building Proprietary Bitcoin Rails

The $30 Trillion Pivot: Why Banks Are Building Proprietary Bitcoin Rails

The retail market remains fixated on daily spot ETF inflows, cheering for wrapper products as if they represent the pinnacle of adoption. This focus is misplaced. The real structural revolution is not occurring on the trading desks of BlackRock, but in the back-office plumbing of Global Systemically Important Banks (G-SIBs). Citigroup’s initiative to integrate Bitcoin into a $30 trillion asset ecosystem by 2026 is not a "crypto strategy"—it is an industrialization strategy.

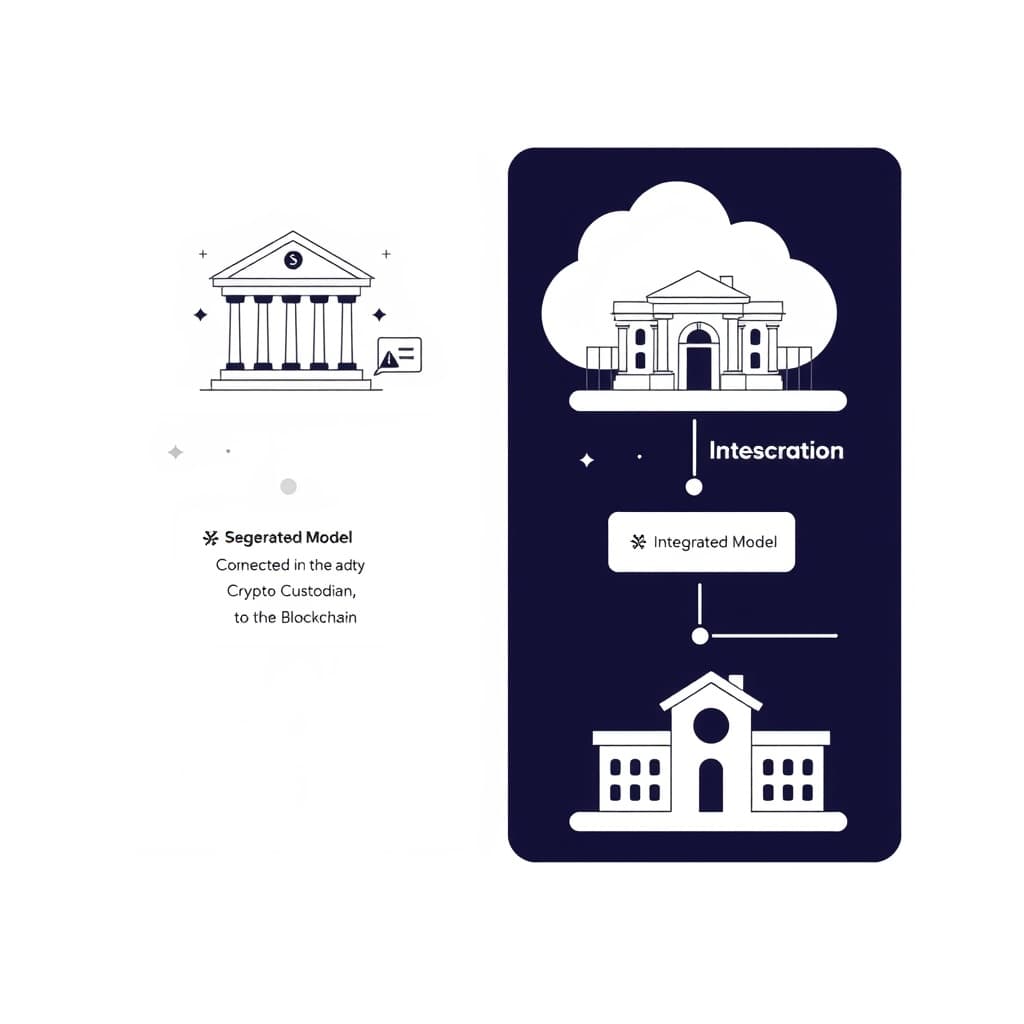

We are witnessing the end of the "crypto island" era. For the last decade, digital assets lived in a segregated parallel universe, connected to traditional finance only by fragile API bridges. The new mandate is Legacy-Integrated Custody Rails: the direct fusion of distributed ledgers with the core banking systems that handle sovereign debt and fiat clearing.

This pivot is driven by a single, ruthless constraint: capital efficiency. In the current high-rate environment, leaving assets in a segregated digital wallet where they cannot be instantly rehypothecated or used as cross-margin collateral is a balance sheet error banks can no longer afford.

Dismantling the Third-Party Intermediary Model

For years, banks relied on a "rented" infrastructure model. They utilized sub-custodians like Metaco, Fireblocks, or partnerships with crypto-native exchanges to offer clients exposure. That era is ending. The friction of reliance has become a systemic risk that risk committees are no longer willing to tolerate.

When a bank relies on an external API for custody, settlement finality is at the mercy of the vendor’s uptime and the API’s latency. In high-frequency traditional markets, milliseconds dictate arbitrage and liquidity; in crypto, the delay between a bank's internal ledger update and the blockchain confirmation creates a "reconciliation gap."

The API Gap and Settlement Risk

In the segregated model, if a client wants to borrow against their Bitcoin holdings, the bank must verify the assets with the third-party custodian, lock them, and then issue the loan. This process involves multiple counterparty checks. By building proprietary rails, banks eliminate the API gap. The Bitcoin sits on a node controlled directly by the bank's core ledger.

This shift allows for atomic settlement between fiat and crypto within the bank's own walled garden. If the asset and the liability sit on the same proprietary stack, the bank can offer instant liquidity against Bitcoin without waiting for external confirmations.

Map of Incentives: The Shift to Proprietary Rails

Citigroup’s Protocol: Merging Bitcoin with Core Banking

Citigroup's roadmap to 2026 is not arbitrary. It aligns with the final implementation phases of Basel III standards regarding the prudential treatment of cryptoasset exposures. To hold Bitcoin on a balance sheet without incurring prohibitive capital requirements, banks must demonstrate absolute control and risk management capabilities that third-party vendors struggle to guarantee legally.

Treating BTC Like Treasuries

The ultimate goal of Legacy-Integrated Custody Rails is to treat Bitcoin exactly like a U.S. Treasury bond. In a unified ledger approach, the bank’s internal database records the ownership of the Bitcoin, while the proprietary node manages the on-chain reality.

This integration allows the bank to leverage Bitcoin for intraday liquidity. Currently, banks use Treasuries to manage liquidity needs via repo markets. By integrating Bitcoin directly into the core banking stack (connected to payment rails like FedWire or SWIFT), Bitcoin can theoretically be used in similar internal liquidity pools, provided the regulatory capital buffers are met.

The 2026 Timeline and Technical Readiness

The 2026 target suggests that Citigroup is building a "Digital Asset Core" that runs parallel to its legacy mainframe. This involves:

- Node Infrastructure: Running enterprise-grade Bitcoin and Ethereum nodes inside the bank's firewall.

- Ledger Abstraction: Middleware that translates blockchain UTXOs (Unspent Transaction Outputs) into standard ISO 20022 financial messaging formats that legacy systems understand.

Cold Storage Meets Regulated Insolvency Protection

The crypto ethos of "not your keys, not your coins" is valid for individuals but legally insufficient for institutions. For a pension fund, the mantra is "not your bankruptcy-remote trust structure, not your assets."

Bankruptcy Remoteness

If a crypto exchange fails, customer assets are often tied up in the bankruptcy estate, treating depositors as unsecured creditors. We saw this catastrophe with FTX and Celsius.

Banks are building rails to ensure bankruptcy remoteness. Under this legal structure, the Bitcoin held in custody is legally segregated from the bank’s own balance sheet. If Citigroup were to fail, the assets in these proprietary custody rails would theoretically remain the property of the client, untouchable by the bank’s creditors. This legal certainty—backed by centuries of case law rather than a User Agreement—is the product banks are actually selling.

Institutional HSM Clusters vs. MPC

While crypto-natives favor Multi-Party Computation (MPC) for its flexibility, legacy banks lean toward Hardware Security Modules (HSMs) operating at FIPS 140-2 Level 3 standards.

- MPC: Shards the key across multiple devices/servers. Good for speed and operational flexibility.

- HSM Clusters: Physical hardware devices kept in air-gapped bunkers. Banks prefer this because it aligns with existing hardware security standards used for ATM networks and interbank clearing.

By building proprietary rails, banks can integrate these HSMs directly into their existing cybersecurity perimeter, rather than trusting a third-party vendor's cloud-based MPC solution.

The Tokenization Endgame: Beyond Just Bitcoin

Bitcoin is merely the Trojan Horse. The infrastructure Citigroup and its peers are building is not designed solely for a $1 trillion asset class; it is designed for the $100 trillion market of Real World Assets (RWA).

Bond Issuance and Settlement

Once the rails are established for Bitcoin, the same infrastructure will host tokenized bonds, equities, and real estate. The cost of building a proprietary node network is difficult to justify for Bitcoin custody fees alone. However, if that same network can settle a corporate bond issuance in T+0 (instant) rather than T+2 (two days), the capital savings are astronomical.

This creates an existential threat to crypto-native custodians. If a bank can offer custody, trading, lending, and issuance of both crypto and tokenized securities on a single platform, specialized crypto custodians become redundant. The value proposition shifts from "we understand the blockchain" to "we understand the law and liquidity."

The End of "Crypto Banking"

The era of "crypto banking" as a separate vertical is effectively over. By 2026, digital assets will likely be just another line item on a legacy ledger, indistinguishable in the back office from Eurobonds or Gold futures.

For the decentralization purist, this is a defeat; the intermediaries are not being removed, they are simply upgrading their software. For the institutional investor, however, this is the necessary standardization that turns a speculative bet into a collateralizable asset. The $30 trillion pivot is not about adoption—it is about absorption.

FAQ

Why are major banks moving away from partners like Metaco or Fireblocks? While technology partners remain useful for software licensing, G-SIBs prefer owning the entire risk stack. Reliance on external vendors introduces "vendor lock-in" and counterparty risks. By owning the rails, banks ensure absolute control over compliance, liquidity, and settlement timing without relying on a third party's operational stability.

How does legacy integration differ from holding crypto on Coinbase? Legacy integration connects the asset directly to the bank's fiat liquidity engines and clearing networks. On Coinbase, your Bitcoin is isolated from the broader banking system. In a legacy-integrated model, that Bitcoin can theoretically be used to secure a line of credit or collateralize a trade instantly within the same institution, reducing capital drag.

Sources

- Bank for International Settlements (BIS) - Basel III: The Global Regulatory Framework

- [Citigroup - GPS: Money, Tokens, and Games](https://ir.citi.com/gps/8o%2B1Jz3%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%2B%2F%

Related

View all →

Crypto

Circle's Native Gas Abstraction: How Eliminating Network Fees Rewires Crypto Architecture

March 27, 2026

...

Crypto

When TradFi Meets Stablecoins: Inside the Circle and Mastercard Infrastructure Play

March 13, 2026

...

Crypto

The Great Replatforming: Why LSEG’s Blockchain Pivot Signals the End of T+2 Settlement

February 20, 2026

...