The Hong Kong Backdoor: Unpacking Cross-Border AI Venture Arbitrage

While Washington and Beijing are ostensibly constructing digital firewalls, global capital is busy digging tunnels. The narrative of a complete "decoupling" in the technology sector is, at best, a geopolitical fiction and, at worst, a dangerous blind spot for allocators. The reality is a sophisticated game of Cross-Border AI Venture Arbitrage, where US Limited Partners (LPs)—driven by the fear of missing the next ByteDance-scale AI outcome—are utilizing Hong Kong-based Special Purpose Vehicles (SPVs) to bypass outbound investment restrictions.

This is not merely about finding loopholes; it is a systematic restructuring of capital flows designed to maintain exposure to Shenzhen’s generative AI ecosystem while technically adhering to the letter of the US Treasury’s regulations. The mechanism relies on "capital leakage," where funds originate in New York or Menlo Park, wash through tax-neutral offshore jurisdictions, and re-emerge in Hong Kong as "local" capital ready for deployment.

Structuring the Loophole: The Hong Kong SPV Mechanism

The architecture of modern evasion is built on the legacy of the Variable Interest Entity (VIE), but adapted for an era of active hostility. Where the traditional VIE was a tool for Chinese companies to list abroad, the new Hong Kong SPV is a tool for Western capital to enter China anonymously.

Layering Ownership Through Multi-Tiered VIEs

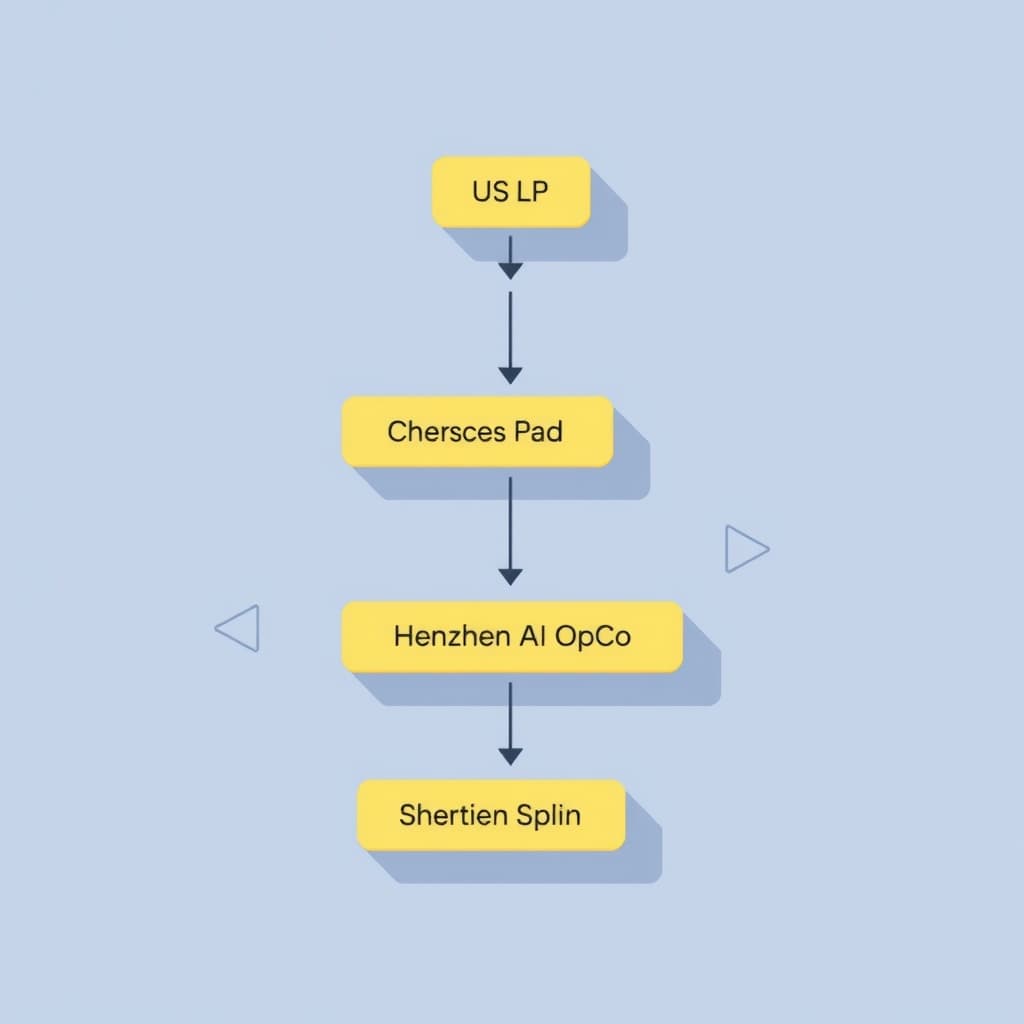

The primary method involves a "double-blind" structure. A US-domiciled venture fund does not invest directly in a Chinese AI startup. Instead, it invests in a Cayman Islands or British Virgin Islands (BVI) "Feeder Fund." This feeder fund aggregates capital from various global sources—Europe, the Middle East, and the US—effectively diluting the "US person" status of the capital pool below the thresholds that typically trigger immediate scrutiny.

This Cayman entity then pushes capital into a Hong Kong SPV. Under Hong Kong law, the beneficial ownership registers are less transparent to US regulators than direct equity stakes. The Hong Kong SPV then enters into contractual arrangements—not direct equity ownership—with the mainland Chinese AI operating company (OpCo). These contracts grant the SPV economic rights (profits) and control without technically holding shares that would appear on a cap table subject to an audit by the Committee on Foreign Investment in the United States (CFIUS) or its outbound equivalent.

The Role of "Blind Pool" Funds

Plausible deniability is the currency of the realm. US LPs are increasingly committing capital to "blind pool" funds managed by GPs based in Singapore or Hong Kong. In these agreements, the LP signs a side letter explicitly stating they do not "knowingly direct" their capital toward prohibited Chinese sectors.

However, the LP agreement often contains broad mandates for "Asia-Pacific Technology," which the GP interprets as a green light for Chinese AI. Because the LP does not approve individual deals (a standard practice in blind pools), they maintain a legal defense against claims that they violated Executive Order 14105. They are simply "passive investors" in a global fund that "happened" to allocate to a Shenzhen Large Language Model (LLM) developer.

The Valuation Gap: Why US Allocators Chase Forbidden Alpha

If the legal risk is existential, the financial incentive must be compelling. The driving force behind this arbitrage is a massive valuation disconnect caused by geopolitical fear.

Arbitraging the Geopolitical Discount

Chinese AI startups are currently trading at a severe "geopolitical discount" compared to their Silicon Valley peers. While a foundational model company in Palo Alto might command a valuation of 50x to 100x forward revenue, a comparable firm in Beijing—possessing similar engineering talent and data access—might trade at 5x to 10x.

Venture capitalists are essentially betting on mean reversion or a localized exit. They argue that even if the company cannot IPO on the NASDAQ, a domestic listing in Shanghai or an acquisition by a Chinese tech giant (Alibaba, Tencent) would still yield a 10x return due to the suppressed entry price.

The Liquidity Dilemma: High Growth vs. Exit Blockades

This strategy creates a "Roach Motel" scenario: capital checks in, but it cannot check out easily. The traditional exit route—a US IPO—is dead. The Hong Kong Stock Exchange (HKEX) remains a viable option, but liquidity there has been anemic compared to US markets.

Investors are banking on secondary market liquidity. The thesis is that once the startup matures, the early US investors will sell their stakes to state-backed Chinese guidance funds or Middle Eastern Sovereign Wealth Funds (SWFs) seeking exposure to China. The table below illustrates the stark contrast in investment environments.

Washington’s Radar: The Reach of Executive Order 14105

The US government is not oblivious to these maneuvers. The Biden Administration’s Executive Order 14105, finalized by the Treasury Department, marks a shift from "monitoring" to "prohibiting."

Defining "Knowingly Directing"

The legal battleground for the next decade will be the definition of "knowingly directing." The Treasury’s Final Rule attempts to close the loophole of passive LP investment. If a US person has authority to make investment decisions, or if the fund is structured specifically to pool US capital for the purpose of evading the order, it constitutes a violation.

However, the burden of proof is high. Regulators must prove that the US LP knew the capital was destined for a prohibited transaction. The multi-layered SPV structures described earlier are designed specifically to break this chain of knowledge. The defense is simple: "We invested in a Cayman fund; we did not direct the GP to buy equity in a prohibited Chinese quantum computing firm."

From Notification to Prohibition

The regulations create a bifurcated landscape. Investments in AI systems designed for military, intelligence, or mass surveillance are prohibited. However, investments in "standard" AI systems (like generic LLMs) may only require notification.

The danger for investors is the fluidity of these definitions. A generic LLM today can be retrained for military logistics tomorrow. If a portfolio company pivots into a prohibited sector, the US investor is trapped. They cannot inject follow-on capital to dilute their stake, nor can they easily sell without triggering a compliance event.

The 2026 Outlook: From Permeability to Hard Bifurcation

Looking ahead, the "grey zone" of arbitrage is shrinking. The path of least resistance suggests a hardening of financial borders.

The Rise of the "Neutral" Clearinghouse

As Hong Kong comes under increasing scrutiny, we are seeing the emergence of the Middle East—specifically the UAE and Saudi Arabia—as the new neutral clearinghouse for AI capital.

Entities like G42 (UAE) or various vehicles under the Public Investment Fund (Saudi Arabia) are positioning themselves as the interface between US technology and Chinese implementation. We expect US venture funds to increasingly route capital through Abu Dhabi or Riyadh rather than Hong Kong to access Chinese markets, using the Gulf's diplomatic neutrality as a shield against US Treasury enforcement.

Map of Incentives: Who Wins and Loses?

-

The Winners:

- Offshore Law Firms: Charging premiums to structure complex, multi-jurisdictional SPVs.

- Middle Eastern SWFs: Acting as the liquidity provider of last resort and collecting fees for being the "neutral" middleman.

- Chinese OpCos: Receiving desperate capital at favorable terms without ceding board control.

-

The Losers:

- US Compliance Officers: Facing impossible forensic tasks to trace "blind" capital.

- Transparent LPs: Public pension funds (e.g., CalPERS) that cannot engage in these dark arts and thus lose access to global diversification.

- Hong Kong Financial Sector: Facing potential secondary sanctions if Washington decides the city is no longer autonomous enough to warrant distinct financial treatment.

Potential Secondary Sanctions

The ultimate risk is that Washington applies the "Huawei model" to Hong Kong financial institutions. If the Treasury Department identifies specific Hong Kong banks or investment firms as systematic facilitators of sanctions evasion for Chinese military AI, they could be cut off from the SWIFT system or the US dollar. This would turn the "backdoor" into a sealed vault, trapping billions in western capital overnight.

Conclusion

The window for cross-border AI venture arbitrage is narrowing as forensic accounting catches up to legal structuring. The "Hong Kong Backdoor" currently offers a seductive path to undervalued assets, but it is paved with existential regulatory risk. Investors must now weigh the suppressed valuations of Chinese tech against the real possibility of asset freezing. The era of seamless global venture capital is over; we have entered the era of capital containment, where every cross-border wire transfer is a potential act of geopolitical defiance.

FAQ

Is it illegal for US investors to hold equity in Chinese AI companies? It depends on the specific technology tier. Under Executive Order 14105 and the Treasury's Final Rule, direct investment in companies developing advanced semiconductors, quantum computing, and specific AI systems for military or mass surveillance end-use is prohibited. Investments in other AI sectors may be permitted but require mandatory notification to the US Treasury.

How do Hong Kong intermediaries facilitate this capital flow? Intermediaries utilize omnibus accounts and layered corporate structures (often involving Cayman or BVI entities) to aggregate capital. This "blind pool" approach obscures the identity of the ultimate US Limited Partners, making it difficult for regulators to trace specific dollars from a US pension fund or family office to a Shenzhen-based AI entity.

What happens if a "permitted" AI investment pivots to military use? This is a critical risk known as "dual-use drift." If a portfolio company shifts focus to prohibited activities, the US investor may be forced to divest their stake, often at a significant loss, or cease all future capital contributions, leading to severe dilution.

Sources

Related

View all →